Reap the Whirlwind: Low Financial Literacy Poses Brand Risk as Newbies Enter the Investing Fray

By Josh Book

The global pandemic has shone a light into many dark corners of current life. While painful, this experience also gives rise to opportunities for awareness, understanding, and, if we’re lucky, collective action. The significant lack of financial literacy in the world marks one of these dark corners. Re-thinking, innovation and decisive action targeted to address this issue would result in meaningful change in the life trajectory for vast numbers of people.

The wealth business is being forced to mobilize in new ways. Wealth executives are positioning to capitalize on the increasing numbers of new investors by improving access to markets and advice, reducing (some) friction in the experience and are seeing increased engagement.

Digital Advice Net Brand Usage

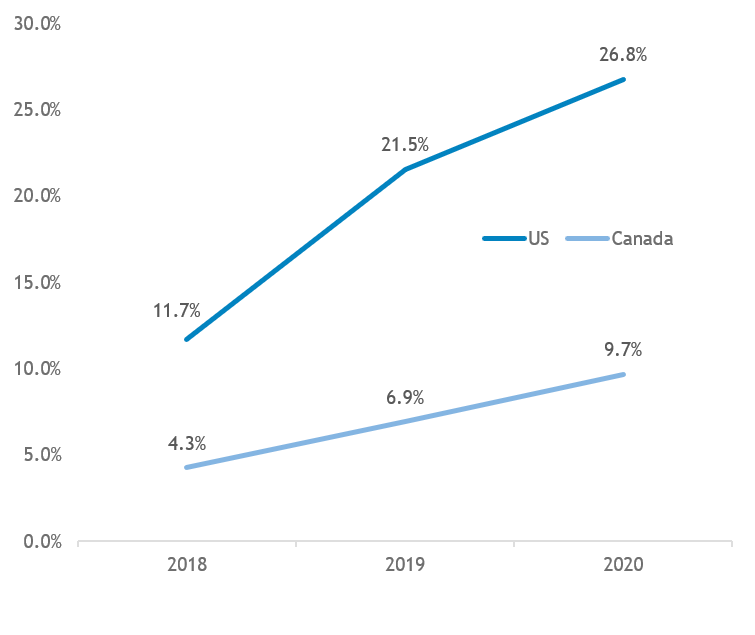

Online Brokerage Net Brand Usage

But there’s a problem…..and if industry leaders (and regulators) don’t consider it there are risks of catastrophic outcomes, even amidst such a boondoggle of opportunity, both in the short and the long term.

A huge number of these investing “newbies” have financial literacy shortcomings. Further, while digital advice has seen record increases in new account openings, a larger percentage of consumers are turning first to online brokerages on the back of industry wide low/no commission trading, GameStop social media hype, and being homebound amidst pandemic.

What happens if, or more likely when, they lose money? What if they’ve been making choices like buying on margin? The concern is that current financial literacy interventions are not enough to help alleviate folks from learning some hard lessons. Sure, people can do what they want. They can also reap the rewards as well as the whirlwind. But the financial services industry goal should be to build innovative on and off ramps for consumers that help them make the best choices for their situations – ask a novice investor to explain risk adjusted returns! Regulators seem inept at distinguishing between the idea of fiduciary duty and allowing firms to arm investors, both experienced and novice alike, with resources and, yes, suggestions upon which to act. But firms themselves need to be more creative in how they build customer journeys such that they provide consumers with options for how to engage in a wealth management experience. We can’t just blame slow moving regulators after all.

Will brands face the wrath of disappointment should newbie investors lose their shirts? This is a real risk. But not because firms did anything “wrong” but because, perhaps, they simply didn’t do enough right. I fear the industry will lose the chance to engage with a vast cohort of jaded consumers who might turn their backs, not only on a brand, but on a chance to improve their financial lives.

The root of the problem is the total and utter lack of attention paid to financial literacy in our schools, our homes, and our communities. Brands will be well served by investing in literacy programs at greater rates if they want to improve their odds at longer and deeper client relationships. Firms like CNBC and Acorns are showing how focus on financial literacy can pay dividends with their “Invest in You. Ready. Set. Grow.” program. ParameterInsights is also focused on this issue and have made an investment in a company called Wealthie Works (www.wealthie.works) which is coming up with innovative ways to engage children in their own financial journey’s. The industry needs to step up and lead the way both within their core wealth businesses but also in their communities.

What kinds of ideas do you have to move the needle on financial literacy in your home, community, or business?